Trapped cash and the inefficient re-cycling of internal liquidity are two issues that treasurers and CFOs often dread hearing while running their treasury operations. Faced with the pressure of making sure capital can be seamlessly channeled between different entities within their organizations, treasurers and CFOs are focused on optimising liqudity management as a priority.

That’s according to Asset Benchmark Research’s (ABR) 2019 Treasury Review of close to 800 participants which found that ensuring access to liquidity was the top treasury goal cited by the participants followed by improving cashflow forecasting and lowering cash flow variability via hedging market risks. Cashflow forecasting in particular has become more important in today’s economic climate considering geopolitical issues such as the trade war between China and the US.

Greater China-based participants differed from the rest of the region as they placed greater importance on managing counterparty risk. This focus on companies working more closely with their service providers comes at a time when treasurers and CFOs are not planning to change their service providers anytime soon. Based on the 2019 Treasury Review findings, 64% of respondents said that they had not changed their primary cash management bank over the past 12 months.

In terms of internal cash management setup, 47% of respondents mentioned that they already had a domestic cash pool setup with another 8% planning to have one in the next six months. Taiwanese companies were the most advanced group when it came to having a domestic cash pool with close to 60% of respondents from the island mentioning that they had already aggregated their bank accounts in order to optimize interest paid and cash visibility.

Despite the treasury goal need for additional liquidity, many respondents were still in the process of centralizing their treasury operations into a regional treasury centre with just over half (52%) of large corporation respondents sharing that they already had or were planning to have a regional treasury centre in the next six months. The likelihood of a regional treasury centre was less likely for mid-cap or small and medium enterprises (SMEs) due to the smaller scale of their operations.

Respondents with established regional treasury centers told the ABR that the centralized setup was primary used for handling bank relations, financial risk management and for coordinating funding requirements. In terms of an Asia-Pacific location for setting up a regional treasury centre, Hong Kong and Singapore were both popular locations with 34% of non-China headquartered organizations opting for Hong Kong as a viable location for a regional treasury centre. Factors such as an advanced market infrastructure, ease of doing business and market liquidity were key considerations for respondents on why they picked a particular location for their regional treasury operations.

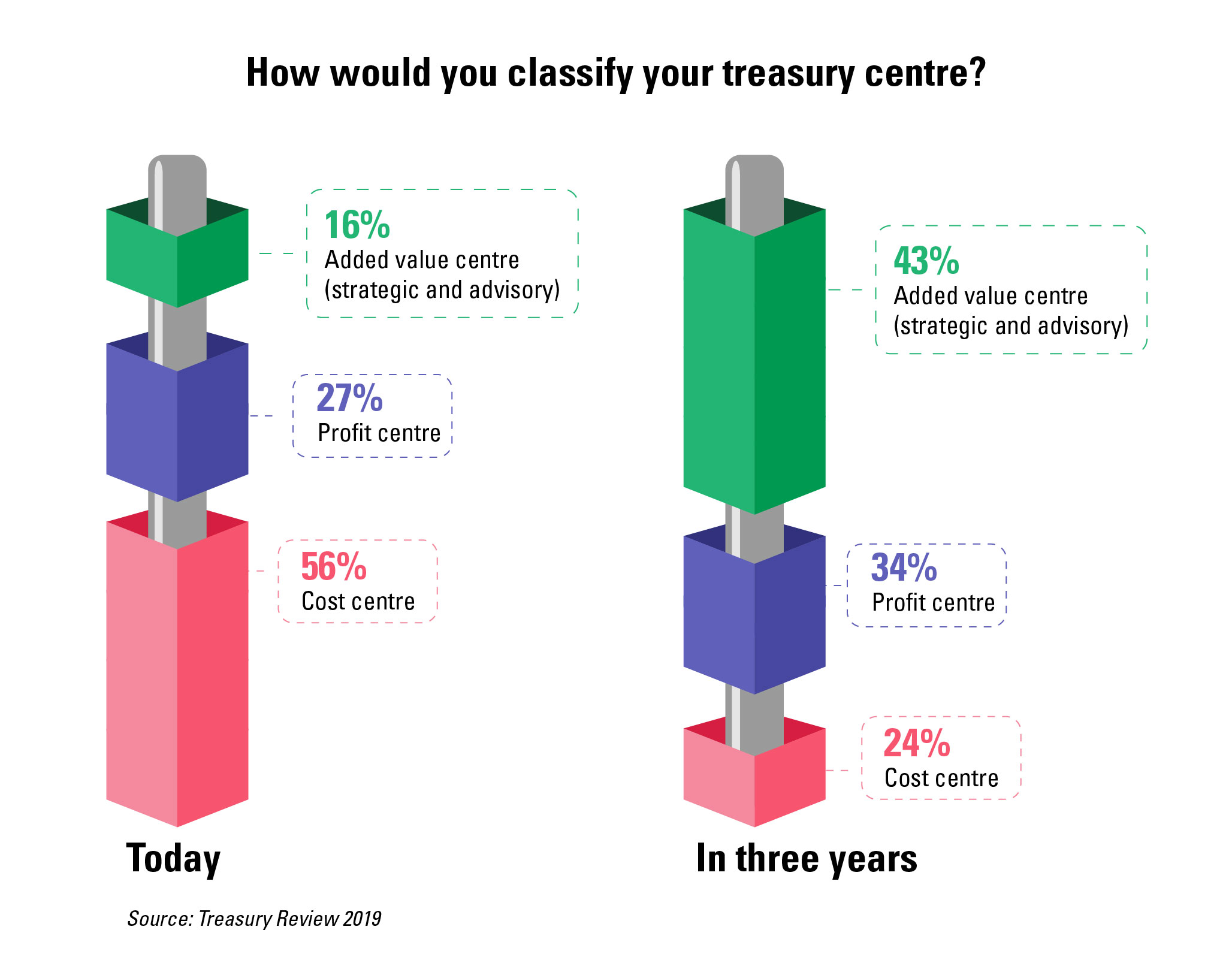

Although currently self-identifying as a cost centre, the majority (77%) of respondents expressed hopes of being either a profit centre or an added value centre in the next three years. They plan for their treasury center to generate alpha on surplus funds in the future or work with upper management on where efficiencies could be realized.

“Around a fifth of the organization’s profitability is contributed by our treasury department. Low yields present a challenge for our investments across the world. We look at benchmarks for investments and our duration of investment tends to be close to 1-1.5 years,” shares a technology company based in India.

Nevertheless, companies surveyed by ABR need more information about short-term corporate investment solutions to generate alpha with only 23% of participants sharing that they had already used such instruments.

About Asset Benchmark Research’s annual Treasury Review

Conducted since 2013, Asset Benchmark Research surveys corporates across Asia on an annual basis to understand the challenges faced by corporate treasurers and CFOs and the solutions they consider best suited to navigate financial markets. In 2019, almost 800 corporate finance representatives participated in the survey, led by decision-makers in Greater China, India and Indonesia. Based on annual turnover, 54% of respondents are small and medium sized enterprises, 27% are mid-caps and 19% large corporations (>US$1bn turnover per annum).

View from Standard Chartered

Ensuring access to liquidity was the top treasury goal cited by the survey participants. This should come as no surprise, as liquidity is the life blood of any organisation and its effective management is critical to meet a company’s objectives. “To have the right amount of the right currency at the right time in the right place to meet a company’s obligations” is possibly the single most important role for Treasury within most organisation.

We see this consistent trend and theme being driven by several factors while manifesting itself in different ways:

Internal funding: Increasingly looking to optimise the use of internal sources of funds to support business growth plans.

Continued focus on risk: Focus on market, counterparty and currency risk because of increased market uncertainty.

Security: Despite large sums of cash on balance sheets, treasurers are remaining cautious when it comes to short-term investment.

Treasury centres and in-house bank structures: Implementation of in-house bank structures in Asia as a complement to pooling structures.

These trends and themes are mainly driven by:

Global sales and supply chains: More corporations now manufacture and trade globally, this creates challenges for cash visibility and control, and results in higher operational costs, a key focus area in this age of “Do more with less".

Rise of the RMB: As an international settlement currency evident in the continued relaxation of cross-border RMB lending guidelines.

Rapidly changing payments environment: Instant domestic and faster cross border payments will be adopted across most OECD and Emerging Markets. This tied to machine learning analytics, will provide more opportunities for forecasting, DSO and DPO optimisation.

In consideration of the high-degree of current and capital account controls and a lack of uniform regulation across the markets of Asia, we typically advocate a combined top-down and bottom-up approach to regional and global liquidity optimisation projects. This approach ensures you begin the process by building appropriate in-country structures, considering local market dynamics and business requirements, while simultaneously identifying opportunities for cross-border liquidity aggregation into your chosen regional and/or global liquidity hub location. Understanding both aspects, allows an optimal or “Best Fit” liquidity solution to be deployed.

Starting with account rationalisation allows you to maximise visibility and control over cash, and also enable more natural liquidity concentration and subsequent liquidity overlays become more optimal and cost efficient. This is a critical success factor from a cost/benefit perspective.

Any multi-market/multi-entity solution will require a hybrid approach and so many MNCs have optimised solutions combining regional interest optimisation structures, in-country and cross-border cash concentration solutions alongside notional pooling structures in the hub locations.

Previously, it was all about centralising liquidity in locations such as London or New York, but the single most significant change over the last few years is the rise of the Asia-centric liquidity structures alongside the increased use of RMB in such structures.

Aside from Asian MNCs, several Western MNC's are also looking at such Asia-centric liquidity models, primarily to support their growing Asian business focus and expansion plans.

This leads us to believe we will see more liquidity structures being developed and implemented in Asia, we will see RMB as a common currency in such structures, and we will also see more “Against the Sun” liquidity models being adopted, supported by the technology that banks, like ourselves, are rolling out. This includes the ability to support extended cut-offs for currencies like USD and EUR in Asia, just in time funding sweeps, enhanced reporting and reconciliation tools, and automated, intelligent and highly configurable liquidity structures. As true partners, banks need to assist Treasurers by creating an “always-on”, “highly automated” and “manage by exception” approach to help them optimise liquidity and do “more with less”.