now loading...

The lifting of quotas for the qualified foreign institutional investors ( QFII ) and RMB-qualified foreign institutional investors ( RQFII ) by Chinese authorities this week is expected to boost the Chinese exchange-traded fund ( ETF ) market in a big way as global investors seek more opportunities in China equities.

Previously, qualified overseas fund managers had to apply for new quotas before they could launch new ETFs under these schemes. The lifting of the QFII and RQFII quotas on September 10 effectively removes one of the biggest single roadblocks to product development in the Hong Kong-China ETF market.

The removal of the quotas will likely revitalize the old QFII/RQFII programs, paving the way for the complementary development of both the Hong Kong and China ETF markets. It also allows global fund managers seeking to reallocate their portfolios, following the inclusion of A-shares in the global MSCI index, more flexibility and opportunities to do so.

The lifting of the quotas came two days before the Hong Kong Exchange ( HKEX ) released a research report that predicts that the growth of the mainland China and Hong Kong ETF markets can be complementary to each other.

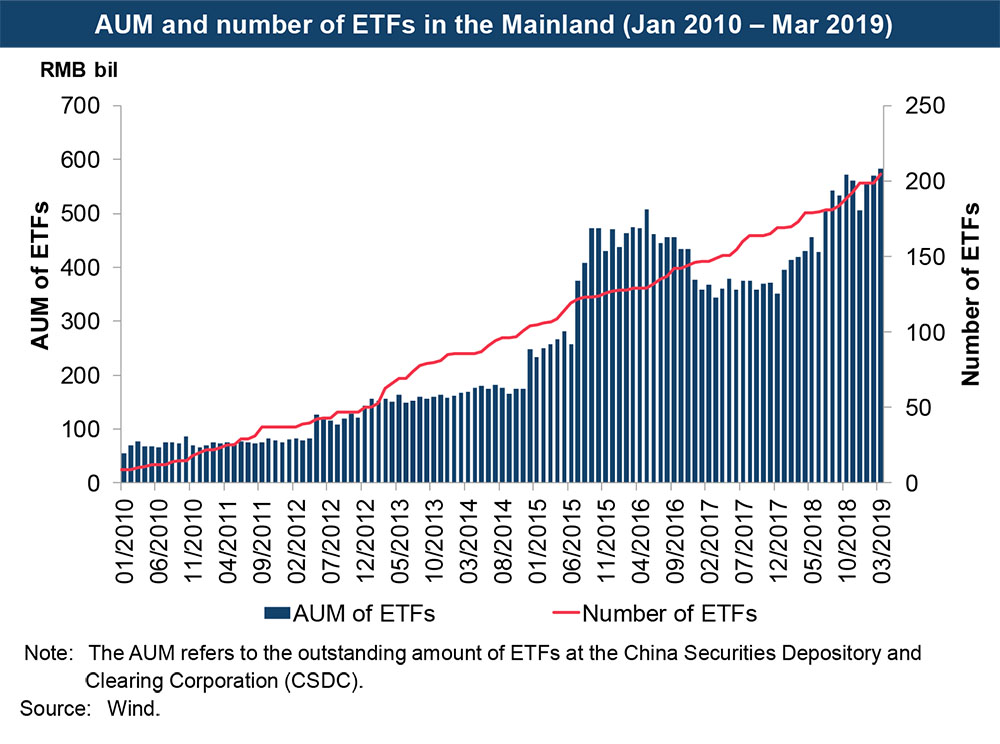

In the mainland, the growing interest in ETFs and the high proportion of ETFs focused on domestic assets may hint at the demand for asset diversification by mainland fund investors.

However, mainland fund investors can only invest in global assets through funds under the QDII scheme and the mutual recognition of funds agreement with Hong Kong, as well as a few cross-listed Japanese ETFs, according to the HKEX report published on September 12.

Hong Kong ETFs can provide complementation because they cover a wide range of Asia-Pacific and overseas equities as well as other global asset classes including fixed income, currency and commodity providing alternative investment options for mainland investors, the report says.

Also, the nature of Hong Kong’s ETF market which is dominated by global institutional investors could complement the nature of China’s ETF market which is dominated by retail investors. Retail investors account for about 86% of the turnover value in the A-share market in 2018.

Although Hong Kong already has a well-developed ETF marketplace with a wide range of asset classes covering mainland and global assets, the range of mainland asset classes is still limited.

About a half of Hong Kong-listed A-share ETFs, for example, track the popular A-share indices in the mainland. Out of 25 A-share ETFs as of end-June 2019, 8 ETFs were tracking the CSI 300 Index and 4 ETFs tracking the FTSE China A50 Index. In comparison, mainland A-share ETFs not only track the headline indices, but also indices of different sectors, ownership, and smart betas.

This means that more diversified product composition in the Hong Kong ETF market, through providing access to mainland ETFs for example, could contribute to attracting new investors worldwide, according to the report.

“The Hong Kong ETF market is a door to global investment, particularly for mainland investors. It offers products on diversified asset classes from global markets and a well-established institutional investor base to support market liquidity,” the report says.